Total return futures come into focus due to 2020 market uncertainty

EQD Research

By Russell Rhoads, original content published on EQD

Several financial market dislocations associated with heightened equity market volatility impacted trading earlier this year. This market activity attracted new traders to total return futures (TRFs) as the relationship between short-term and long-term repo rates fell outside of historical norms. Also, there were firms finding total return futures a viable market to maintain or even increase their equity market exposure. TRFs offer benefits associated with both total return swaps (TRS) that trade OTC and exchange listed equity index futures. Both instruments offer holders the theoretical total return associated with owning the equities that comprise and index, including dividends. Euro Stoxx 50 Total Return (TESX) futures replicate the payoff of a total return swap in a transparent and cost-efficient way.

How does a trf allow repo trading? Generating alpha through equity repo exposure has been a common strategy for over a decade. A typical trade will purchase long-dated and sell near-dated equity repo. Increased equity market volatility creates more opportunities to trade the repo curve as spreads widen out in response to concerns about short term equity market performance. We turned to market participants for a little more insight into TESX trading activity in 2020. When a trade occurs in a TRF, the short counterparty will need to purchase shares of the companies that make up the underlying index to hedge their exposure. Because they hold physical shares the short TRF counterparty will receive dividend payments and have a tax liability associated with this income. Additionally, the short who has hedge with physical shares is obligated to pay pre-tax dividends to the long holder of the TRF. The TRF spread represents how much it costs the short counterparty holding securities to hedge their risk associated with exposure to the underlying total return index. The result is that the TRF spread is a combination of the pure repo rate and seller’s cost of paying dividends.

It is not just buy-side market participants that are turning to total return futures. Leading global market making firm Optiver recently added Euro Stoxx 50 Total Return (TESX) futures to the suite of products where it acts as a market maker. Hans Hakkenberg, Senior Trader at Optiver, sums up trading activity in early March, “In March the downticks on global stock markets caused by Covid 19 and lockdowns resulted in massive repo and dividend exposures on the books of structured products issuers. Traditionally they hedged their exposures using longer term synthetics. Over the past few years, the trend was towards hedging using dividend futures and TRFs. The crisis earlier this year accelerated this trend as liquidity in synthetics alone was not sufficient to absorb the market supply. Besides dividend futures and synthetics, we recently started market making TRFs. We notice good volumes and healthy liquidity with structured retail issuers typically facing D1 desks and hedge funds.”

The TRF term structure is typically upward sloping and the futures pricing is a function of the repo term structure. Different types of market participants will dominate the activity along different parts of the term structure. The short end of the repo curve is driven by the supply and demand related to the physical shares. In March negative demand resulted in sell-off in shares. The long end of the repo curve is influenced by changes in exotic flows, such as forwards related to the issuance of long-dated structured products.

Natasha Sibley, Portfolio Manager at Janus Henderson noted, “The extreme steepness of the repo curve seen in March and April provided great opportunities for investors. The demand for short equity exposure at the front end of the curve, driven by protection buyers and momentum strategies, pushed the short-term repo rate higher while the longer-dated rates moved lower with hedging demands from increasing structured product deltas. Although the levels have retraced since the Q1 stress, we still like this trade as the forward-looking carry remains elevated, but the persistent high volatility of the underlying equity market highlights the need for a truly delta neutral position.”

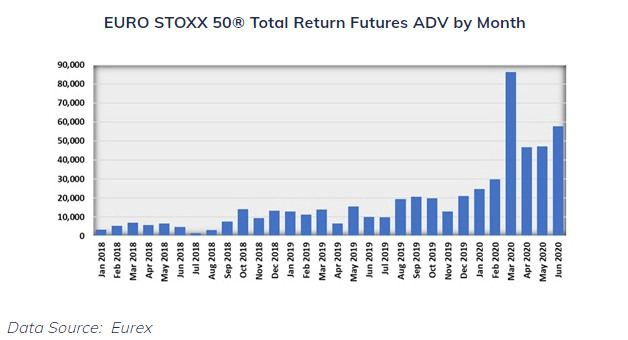

The market activity in March that pushed short-term repo rates higher and long-term repo rates lower created short-term trading opportunities that resulted in the dramatic increase in TESX futures volume. Traders were able to use calendar spreads to eliminate any equity market price risk to benefit when relative repo rates shifted back to historically normal levels. In just a period of weeks it appears traders were able to enter and exit calendar spreads with solid profits earlier this year.

Average daily volume in March 2020 was almost three times the previous month’s figure. Post March, many listed equity derivative markets experienced a drop in volume to levels lower than just before the equity market sell-off. However, TESX futures volume has remained at higher levels. This is a testament to the unique benefits offered by total return futures along with market participant satisfaction with their March 2020 experience in the TESX futures market.

In addition to repo related, calendar spread strategies other uses of total return futures include delta one replacement and managing dividend risk. Longer-dated total return futures are a preferred alternative to traditional price-only index futures as a TRF avoids rolling positions to maintain exposure. This eliminates the risk associated with having to roll quarterly futures positions and adds to the longer-term certainty of the performance of a delta one strategy using futures.

When the market experienced heightened volatility in March 2020, there were concerns with respect to future dividend payments by constituents of the Euro Stoxx 50. Also, this uncertainty coincided with the time that firms holding traditional quarterly equity futures contracts roll their positions from March to June. Since total return futures have less price sensitivity to dividends, when compared to traditional price index futures, there was an increase in trading of TESX futures expiring in Dec. 2020 and Dec 2021 which is believed to be a function of traders shying away from rolling positions at that time.

With more firms aware of how repo rate dislocations may be taken advantage of using total return futures, this market should continue to maintain the strong volume trends that resulted from early 2020 equity market volatility. Hedge funds and asset managers are exploring repo trades as well as looking to using TRFs for more traditional delta one positions to enhance returns and also manage equity market exposure. The entry of leading market makers such as Optiver is another endorsement of TRFs and specifically TESX futures. In addition to being an endorsement of this market, it also assures TESX liquidity when it is most needed by market participants.

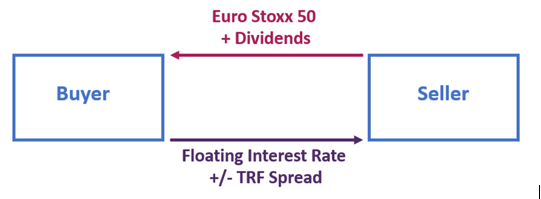

The box diagram below illustrates the cash flows associated with TESX buyers and sellers. The holder of Euro Stoxx 50 Total Return Future receives the Euro Stoxx 50 index price performance plus the pre-tax value of any dividends paid by components of the Euro Stoxx 50. In return, the buyer pays to the seller a benchmark rate plus a spread based on the factors laid out above.