Building resilience in EU equity markets

Why Does Trading Stop During Primary Market Outages

In complex systems like financial exchanges it is inevitable that issues and even outages occur from time to time. However, why do outages on the primary market cause trading to stop on other exchanges? Why aren’t volumes moving to MTFs? What are the downstream effects of these systemic fragilities and what can be done to improve them? We hope to spark a discussion on the steps needed to build resilience in EU equity markets which would undoubtedly benefit all investors and European capital market participants.

Recently there have been a number of unexpected technical failures on European primary (listing) exchanges. While MTFs like Cboe Europe or Turquoise remained open and functioning, trading did not migrate to those venues, it simply stopped. While the reasons for this are complex, we believe it highlights important systemic fragilities in the European capital markets that should be addressed.

Like any complicated technical infrastructure, financial exchanges occasionally encounter system failures that results in the temporary closure or limited functioning of the exchange. While these outages should of course be minimised, they are to some extent inevitable. European capital markets have a number of venues for trading equities so an issue on one exchange should – in theory at least – simply result in trading occurring on other venues.

However, in practice, we do not see this occurring when a primary market has an issue. Instead, trading largely halts across Europe in the equities with their primary listing on the directly affected exchange. Is this a desired feature of European capital markets or a sign that there is a lack of resilience in the market structure? In this paper we explore some of the drivers of this phenomenon and highlight potential areas for improvement.

Importantly, we view this phenomenon as a broad systemic issue. Therefore, change would require the concerted effort of many stakeholders – with this paper we hope to spark discussion amongst those stakeholders and look forward to further engagement across the industry.

Some Data

In the past two major primary exchange outages (Euronext on 19 October 2020, Xetra on 1 July 2020), the following shifts in total notional value and relative market shares occurred across the major European lit Markets and MTFs1.

1 Data courtesy of Cboe Global Markets https://markets.cboe.com/europe/equities/market_share/index/cboe/

See Appendix for a fuller discussion of the data

What we see is quite interesting – while one would expect that relative percentage of traded notional done on the affected markets would plummet, it actually barely moved. Instead, overall traded notional in shares with their primary listing on the affected market dropped across all exchanges in Europe. This shows that an outage on the primary market affects trading across the EU, not just on the affected market. A similar effect is observed for other recent exchange outages.

Reliance on the Primary

So why is the European market so reliant on the primary listing venue for trading? With all the complexity that so many exchanges, SIs, dark pools, and other alternative trading venues bring, we would expect them to also provide some resilience, especially given that in other markets with a multiplicity of trading venues (e.g. the United States) such resilience is observed.

We note the following factors:

- Many algos and trading modalities are explicitly pegged to the primary market Best Bid or Offer (PBBO), instead of a European BBO (EBBO)

- This means these algos or modalities (such as those reliant on the reference price waiver) simply cannot function if the PBBO is not available.

- MiFID II directly forces a link to a single market instead of the European system as a whole by linking waivers like the Reference Price Waiver to the Most Relevant Market instead of pan-European volumes

- Diversity and breadth of participants / members remains far higher on the primary markets than MTFs or other alternate venues

- Unlike in, for example, the US, where brokers are largely forced to connect to every exchange due to Reg NMS

- The post trade environment in Europe remains highly fragmented.

- Despite the promises of CCP interoperability, in many cases members have access only to an incumbent exchange-CCP-depository connection, meaning they cannot clear and settle trades done on an alternate venue.

- There is a self-fulfilling expectation that trading stops if the primary is down

- Because this has been the norm for some time now in Europe, broker and market maker algos are programmed to expect trading to dry up during an outage – and therefore stop trading or quoting automatically, ensuring the expectation is met and reinforcing the cycle for the next event.

- Primary markets retain a de facto monopoly on closing auctions and prices

Is This Actually a Problem?

One could ask if this is truly a problem for the financial markets. After all, despite a continued global trend toward longer financial market trading hours (see our previous Insight on this topic) , we do have weekends and holidays where no trading occurs. However, in our view there is a clear difference between scheduled closures that all market participants can plan for long in advance, and an unexpected sudden loss of the ability for effective risk transfer and price discovery. This is especially true when markets are more volatile or news comes out (see our Insight on the damaging effects of this).

Furthermore, unexpected outages and a lack of resilience in the markets have enormous downstream effects, especially when the outage is not handled in an orderly manner. Any outage that effects the closing procedure exacerbates this impact by an order of magnitude. An obvious outcome is the impact on derivatives or funds/ETFs that track the prices of the effected instruments. Without a reliable set of closing prices, ETFs and other funds cannot accurately calculate their NAVs. This means that any trades linked to those NAV prices either cannot occur or must be done using a fall-back price (for which there is no standardised procedure). Similarly, derivatives which settle based on primary market prices cannot settle. In the case of options this has enormous effects; if the settlement is delayed, those parties’ short options have exposure for a longer time than they priced in (and vice versa for those long options).

Therefore, we do believe this is a serious area of concern, and that the industry should work together to improve resilience in these cases.

Proposed Enhancements

As noted earlier, this is a complicated issue and virtually every stakeholder is affected and must therefore be involved in a discussion. However, we do want to highlight some immediate areas of improvement as well as some ideas for industry discussion. We would urge additional collaboration with derivatives exchanges as well.

Immediate Improvements:

We believe the biggest system risk to the markets is unclear and/or inconsistently applied procedures for notification, fall-back and recovery during and following an outage. Therefore, our immediate improvements focus on codification and standardisation of these procedures across the industry.

- Clear and structured communication from exchanges when an outage occurs.

- Currently, exchanges disseminate information in different ways and often differently to different parties.

- As this is critical information to all parties, there should be a standard for information that is adhered to, ideally standardised across all exchanges.

- Halting of market data or trade flow

- Exchanges must also clearly and completely halt their flow of market status, market data, etc. when trading is halted due to an outage

- Standardised reopening procedures when an outage occurs

- All exchanges should follow a standardised procedure and timings so that participants know exactly what and when to expect changes

- Create an industry-wide backup plan for the close

- We would suggest that, with the recent growth in alternative (closing) auction mechanisms across European venues, that running a closing auction on one (and only one) of these venues should be the procedure

- Barring this however, there should be an industry standard fall-back plan for closing prices in the case of a missed closing auction, to ensure the orderly settlement of derivatives contracts, calculation of fund/ETF NAV prices, etc

- Such protocols already exist and are tested regularly in the United States so many global players will already be familiar with how to handle them2,3.

2http://www.nasdaqtrader.com/content/newsalerts/2017/eta/SIP_Contingency.pdf

3 http://www.nasdaqtrader.com/TraderNews.aspx?id=ETA2020-72

Further Topics for Discussion

We would like to propose that, in addition to working on the immediate principles noted above, the industry discusses the following topics. Ideally these discussions will be organised by collective industry bodies and represent a range of engaged participants.

- How can we avoid the self-fulfilling expectation that trading stops when the primary market is down?

- What protections should exchanges automatically implement to make participants more comfortable?

- For example, tighter price collars, alternative reference points

- What simplifications can brokers put in place in their algos to ensure at least some trading can be facilitated safely?

- For example, using basic limit orders only for those with clear price ideas in mind

- Should protections be different for different client types (professionals vs retail)?

- What do market makers need to be comfortable in continuing to quote?

- Should alternative matching models take a larger role during outages and what changes to their design would be needed to facilitate that?

- Could a Consolidated Tape help in these circumstances?

- What role should regulation play?

- Should there be regulatory intervention to ensure more resilience (perhaps to codify the standards mentioned in the previous section)?

- How do best execution policies get affected?

- Should there be minimum resilience standards adopted for exchanges, brokers, market makers?

- How can we get to full interoperability of CCP/CSDs (or a single utility function)?

Conclusion

We recognise that resilience across the financial markets is a large multifaceted concept that cannot be solved with a single action or a simple solution. However, we do believe there are some clear improvements to be made as well as a number of points that can be discussed and built upon. Given the multitude of execution venues available today in Europe, we believe it is unacceptable to simply stop trading if the primary exchange happens to have a technical issue. We welcome discussion on the topic and look forward to developing improvements that all investors and European capital market participants can benefit from.

Appendix: Data Tables

In this Appendix we present a broader commentary on the notional volume traded and relative market shares of the main European lit markets during two major primary exchange outages; Xetra on 1 July 2020 and Euronext on 19 October 20201.

[1] All data is courtesy of Cboe Global Markets European Market Share website on https://markets.cboe.com/europe/equities/market_share/

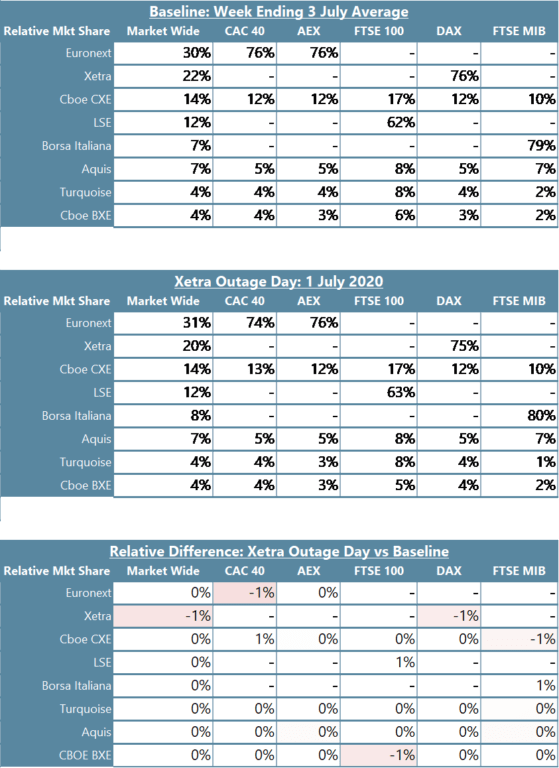

Xetra: 1 July 2020

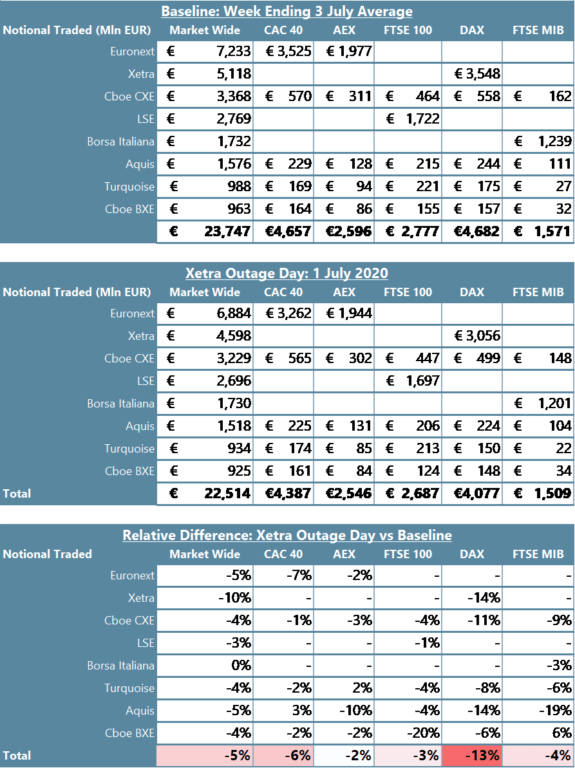

Firstly, as a baseline, we have the average notional traded for the week ending 3 July 2020 as well as the notional traded specifically on 1 July 2020, the day that Xetra suffered a major outage, for the main European lit markets and key blue-chip indices:

While trading volumes on 1 July were down across the board vs the rest of the week, you can clearly see, trading in the DAX (whose constituents have their primary listing on Xetra) was down more. The overall market volume decline could be due to it simply being a quiet day or due to a major part of broad indices like Eurostoxx 50 being closed having a dampening effect on the whole market.

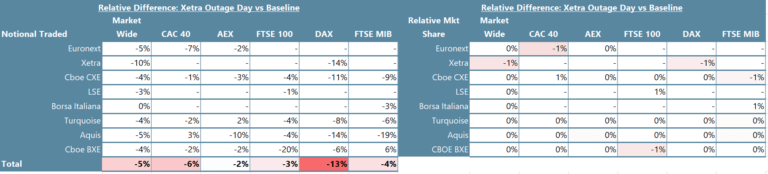

What is really interesting though is the relative market shares of Xetra was essentially unaffected:

Euronext: 19 October 2020

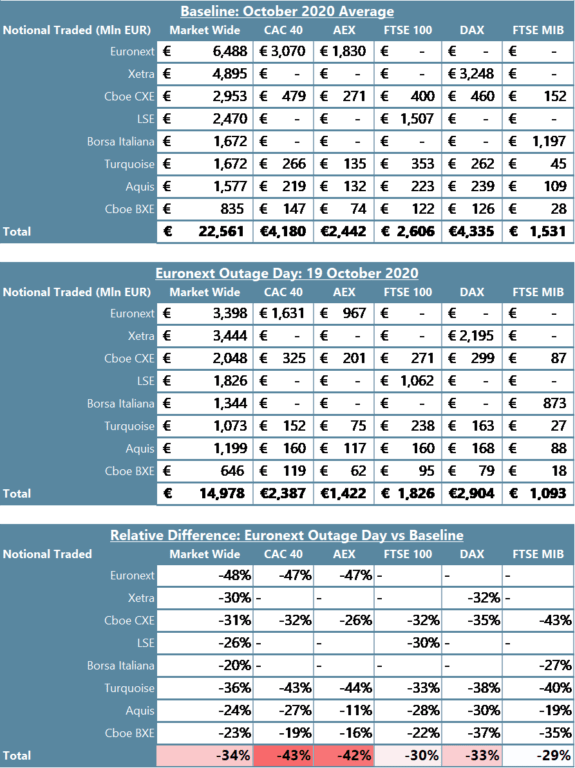

Again, as a baseline, we have the average notional traded for October 2020 as well as the notional traded on 19 October, the day that Euronext suffered a major outage, for the main European lit markets and key blue-chip indices:

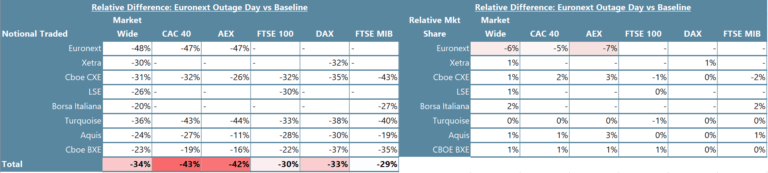

So clearly 19 October was a quieter trading day overall, but as you can clearly see once again, trading in CAC and AEX (whose constituents have their primary listing on Euronext) were down more. The overall market volume decline could be due to it simply being a quiet day (it was the day after 3rd Friday expiration, which is always quiet) or due to a major part of broad indices like Eurostoxx 50 being closed having a dampening effect on the whole market.

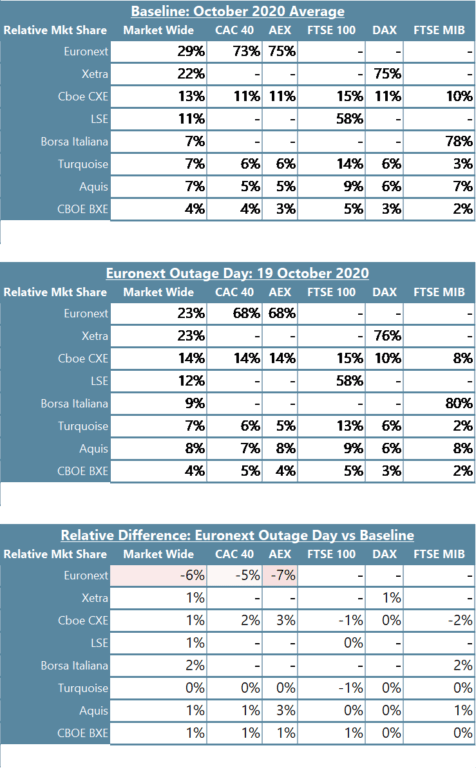

Let’s look again at the relative exchange market shares:

Again, like in the Xetra example, the relative market share of Euronext actually ticked down less than expected given it was closed for nearly half the day. Instead, again, overall traded notional in shares with their primary listing on Euronext simply dropped (more than the broad market).

[1] All data is courtesy of Cboe Global Markets European Market Share website

About Optiver

Optiver is a leading global electronic market maker with over 1000 employees working from offices in Amsterdam, Chicago, Sydney, Shanghai, Hong Kong, Taipei and London.

Through pricing, execution and risk management, we provide liquidity to financial markets using our own capital, at our own risk, trading a wide range of products: listed derivatives, cash equities, ETFs, bonds and foreign currencies. Our independence allows us to objectively improve the markets through pioneering trading strategies and sophisticated technology.

Optiver supports open discussion and debate on all market structure topics that would lead to an improvement of the market. To discuss this paper – or any other market structure topic – reach out to the Optiver Europe Corporate Strategy team.

DISCLAIMER: Optiver V.O.F. or “Optiver” is a market maker licensed by the Dutch authority for the financial markets to conduct the investment activity of dealing on own account. This communication and all information contained herein does not constitute investment advice, investment research, financial analysis, or constitute any activity other than dealing on own account.